Tags

Debt, Debt Payment, delayed gratification, emergency fund, Financial Literacy, Insurances, Investing, Mutual Fund

The question mentioned in the title, is a common question from readers of this blog as well as messages from my Facebook Page and personal account.

The question mentioned in the title, is a common question from readers of this blog as well as messages from my Facebook Page and personal account.

When people started learning about Financial Literacy, they want to start immediately. NEWS that they are hearing as well as different comments that they are reading in the forums triggers them to do so.

Many want to start immediately but due to their debt they think they cannot start investing.

Did you know that you could start investing indirectly even in debt?

Let me explain what I mean with that statement. Well this is how you start investing even in huge debt.

First Pay off your debt, paying your debt is like investing, just imagine if you have paid off your debt earlier than what you expect, you have already earned those interest that was supposed to be given to whom you are in debt.

You can do this in two ways, either increase your cash flow or decrease your expenses. Know the priority.

When everything goes well. It only means that you have already earned from paying off your debt by not giving more interest.

As an example, if you are in debt of Php 100,000 with 20% interest per year. And you paid the Php 100,000 earlier than 1 year let say 6 months, the effective interest will now only become 10% of the capital (20%/12 * 6). So you save the 10% interest which is supposed to be given as part of the interest for the whole year.

Next, since you have already made a decision to pay your debt chances are, you have change your lifestyle and learn about delayed gratification.

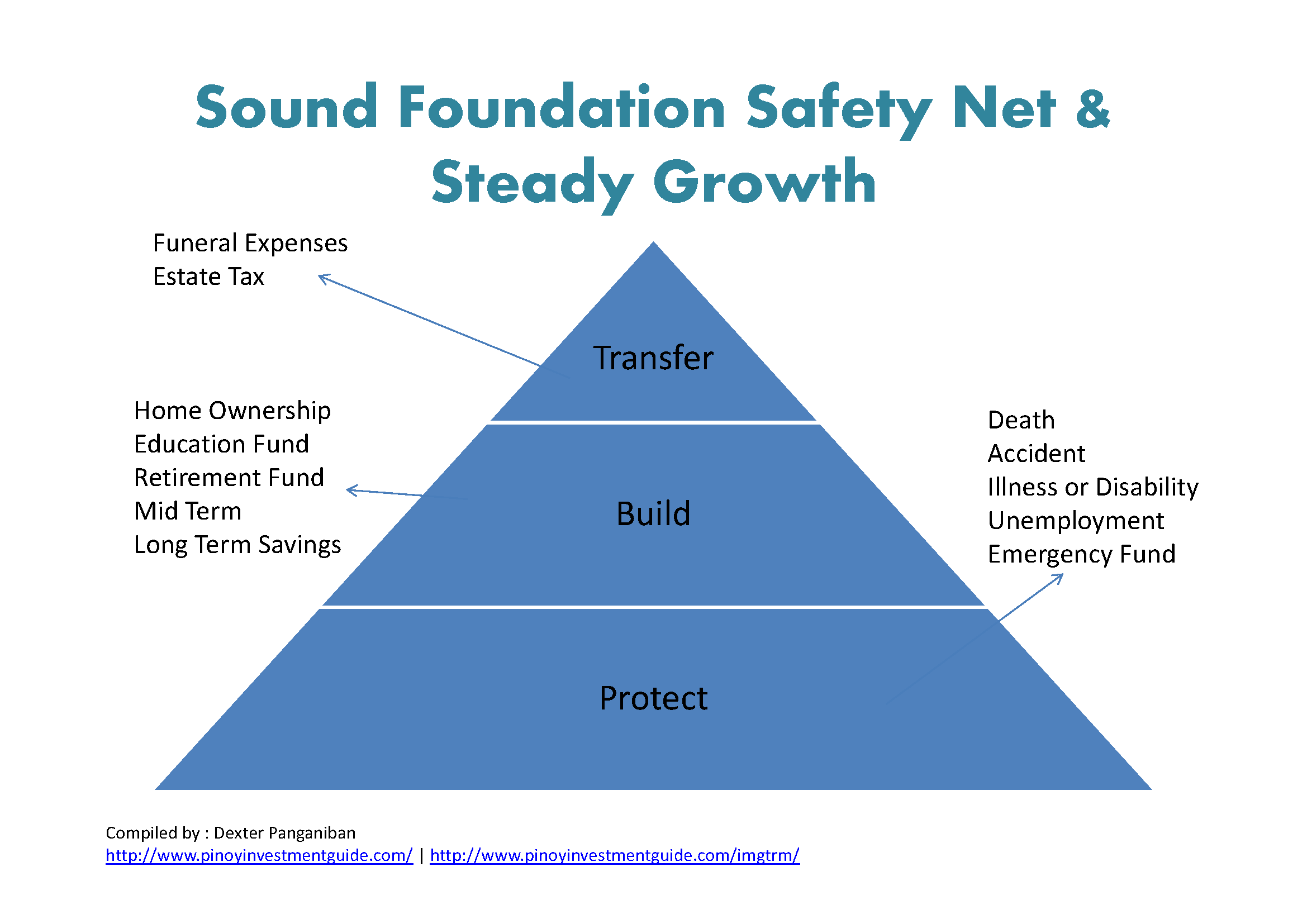

Decide to have a mindset that even you are not in debt you need to continue doing things while you are in debt like delayed gratification, less wants, less social life and more, and now your money that was saved because you have not changed your lifestyle can now be placed in your emergency fund (3 months of your expenses).

Next, after completing your emergency fund, start getting Insurances, Mutual Funds and if you want more, go to the stock market.

Just a friendly advice, don’t start in stock market while in debt, especially if you are in debt, specially in debt with credit card or debt to people which is commonly know us as “5-6”.

There is a very small chance that your earnings in stock market could beat the compounded interest that is being given by those credit card company.

I know that the steps I mentioned above is not easy to do, but if you have your goal for your family and for your retirement I believe that you can do it.

Remember the following verses:

Proverbs 22:7

“The rich rule over the poor, and the borrower is servant to the lender.”

Romans 13:7

Pay to all what is owed to them: taxes to whom taxes are owed, revenue to whom revenue is owed, respect to whom respect is owed, honor to whom honor is owed.

Paying your debt is not easy, it takes courage and determination. So to avoid being servant of lender, pay off your debt and prioritize your payment. First pay those debt that yield the highest interest.